Abstract

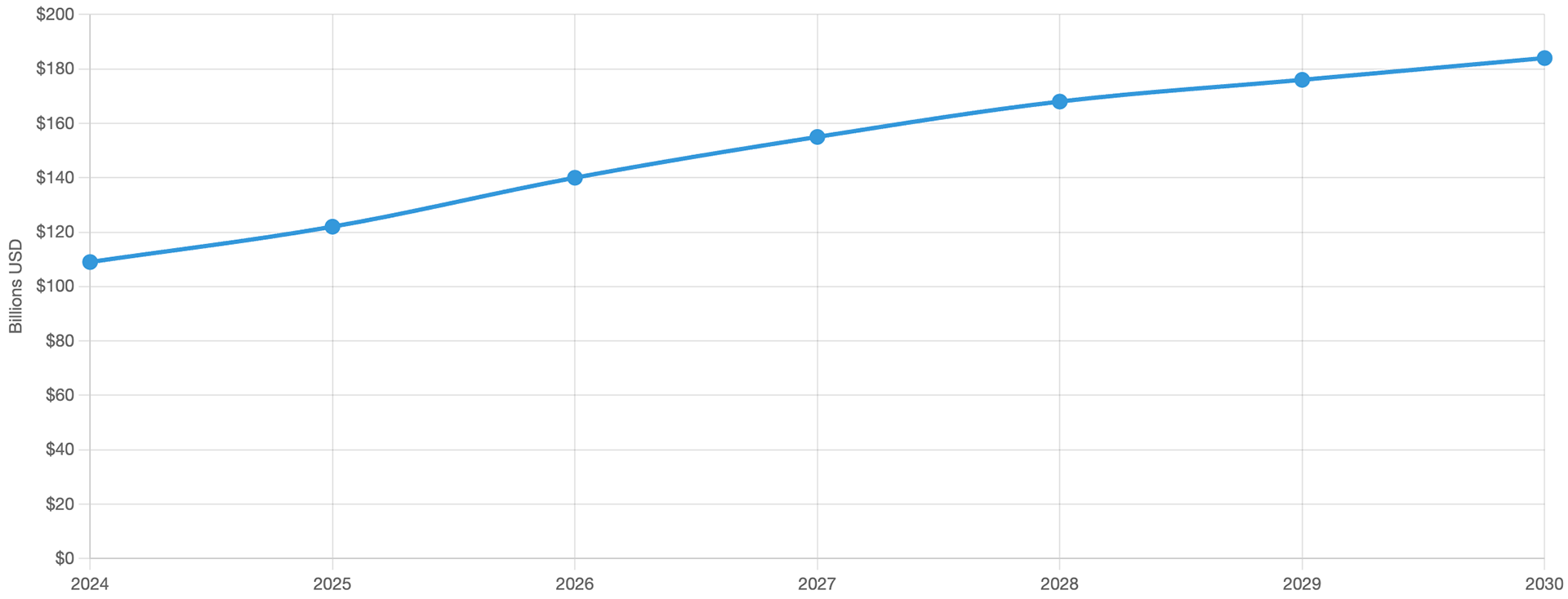

Buy Now Pay Later (BNPL) services have quickly changed from a niche payment option to a mainstream financial product, with the Gross Merchandise Volume (GMV) for BNPL purchases totaling $109.0 billion in 2024 and is expected to reach $184.1 billion by 2030 (Capital One Shopping, 2025). While initial research focused on immediate adoption patterns and short term impacts, emerging evidence reveals profound long-term consequences for both consumer financial health and market structure. This review synthesizes findings, revealing a complex narrative of financial innovation that simultaneously democratizes credit access and increases financial vulnerability. We document how BNPL's initial promise of interest-free convenience evolves into persistent debt cycles for some users. At the market level, we trace BNPL's disruption of the $1.2 trillion consumer credit industry, documenting a 20% cannibalization of credit card revenues and fundamental shifts in merchant pricing strategies. Our analysis projects three scenarios for 2030: regulatory containment limiting growth to $250 billion, market maturation reaching $600 billion with consolidated providers, or full financial integration exceeding $1 trillion in transaction volume. These findings hope to carry implications for policymakers navigating between innovation and consumer protection, as well as merchants recalibrating pricing strategies in an increasingly complex credit landscape.

Global BNPL Market Growth (2024–2030)

Transaction Volume in Billions USD

Source(s): Demand Sage (2025); Capital One Shopping (2025); Bian, Cong, & Ji (2024) for macro context.

Part I: BNPL's Evolution and Promise

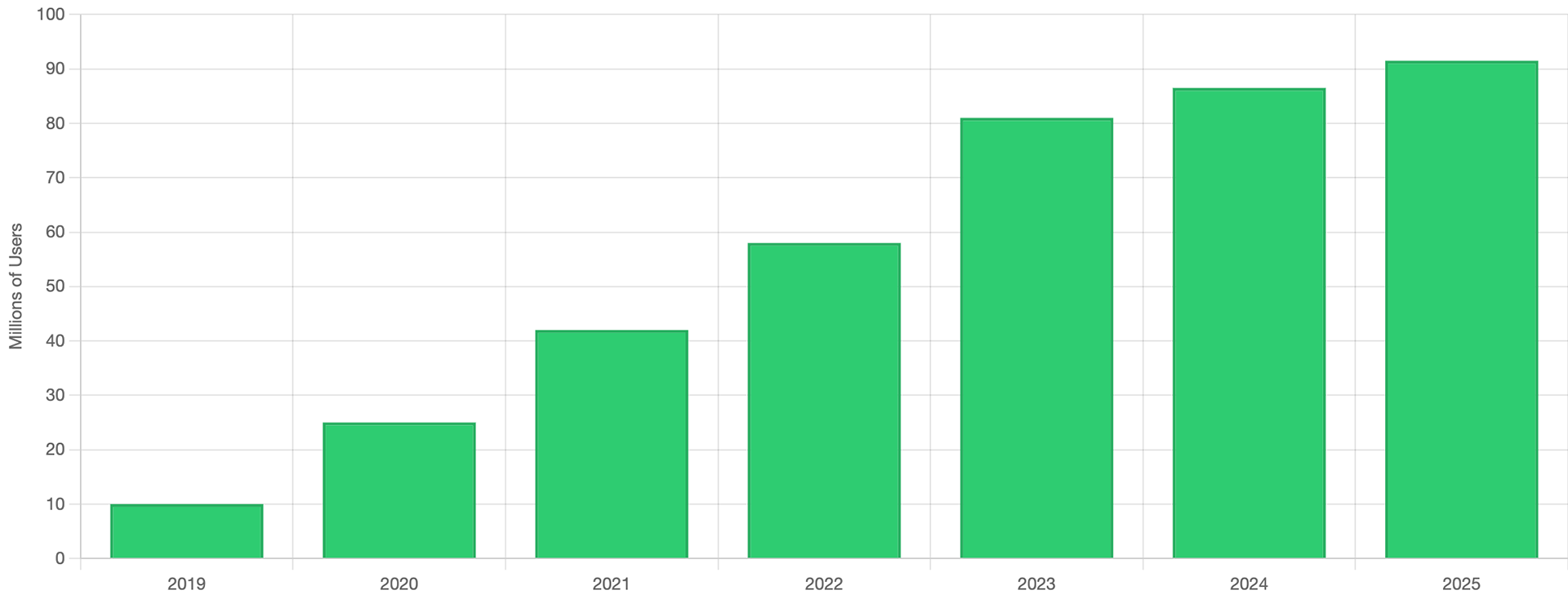

The story of Buy Now Pay Later begins not in Silicon Valley boardrooms but in the fundamental human desire to smooth consumption over time. What distinguishes modern BNPL from its historical predecessors, such as layaway plans, installment options and credit cards, is its seamless integration into digital commerce and its psychological reframing of debt as a budgeting tool. As Berg et al. (2024) demonstrate in their merchant-perspective analysis, BNPL represents "a key innovation in consumer payments" that fundamentally alters the traditional relationship between price, payment, and purchase timing. In their merchant-backed studies they showed that BNPL increases sales by 20%, driven by low-creditworthiness customers and products where market power is larger. BNPL thereby significantly increases merchant profitability. The rapid rise of BNPL services between 2019 and 2024 represents one of the fastest adoptions of a financial innovation in modern history. BNPL usage in the United States alone grew from 10 million users in 2019 to 86.5 million in 2024, representing a 765% increase that outpaced even the adoption curves of credit cards in the 1960s and online banking in the 2000s (Capital One Shopping, 2025). This explosive growth occurred against a backdrop of historically low interest rates, pandemic driven e-commerce acceleration and generational shifts in attitudes toward traditional credit products.

BNPL User Growth in the United States

Number of Users (Millions)

Source(s): Capital One Shopping (2025)

The initial value proposition appeared amazing, consumers could split purchases into four equal, interest-free payments while merchants enjoyed increased conversion rates and higher average order values. Early evidence supported these benefits. Kumar et al. (2024) found that BNPL adoption led to a 6.42% increase in online spending, while Berg et al. (2024) documented even more dramatic effects, with merchants experiencing a 20% increase in sales driven primarily by low-creditworthiness customers. The average BNPL transaction of $135 over six weeks seemed to represent a sweet spot which was large enough to matter for budgeting purposes but small enough to avoid the debt trap associations of traditional credit (Demand Sage, 2025).

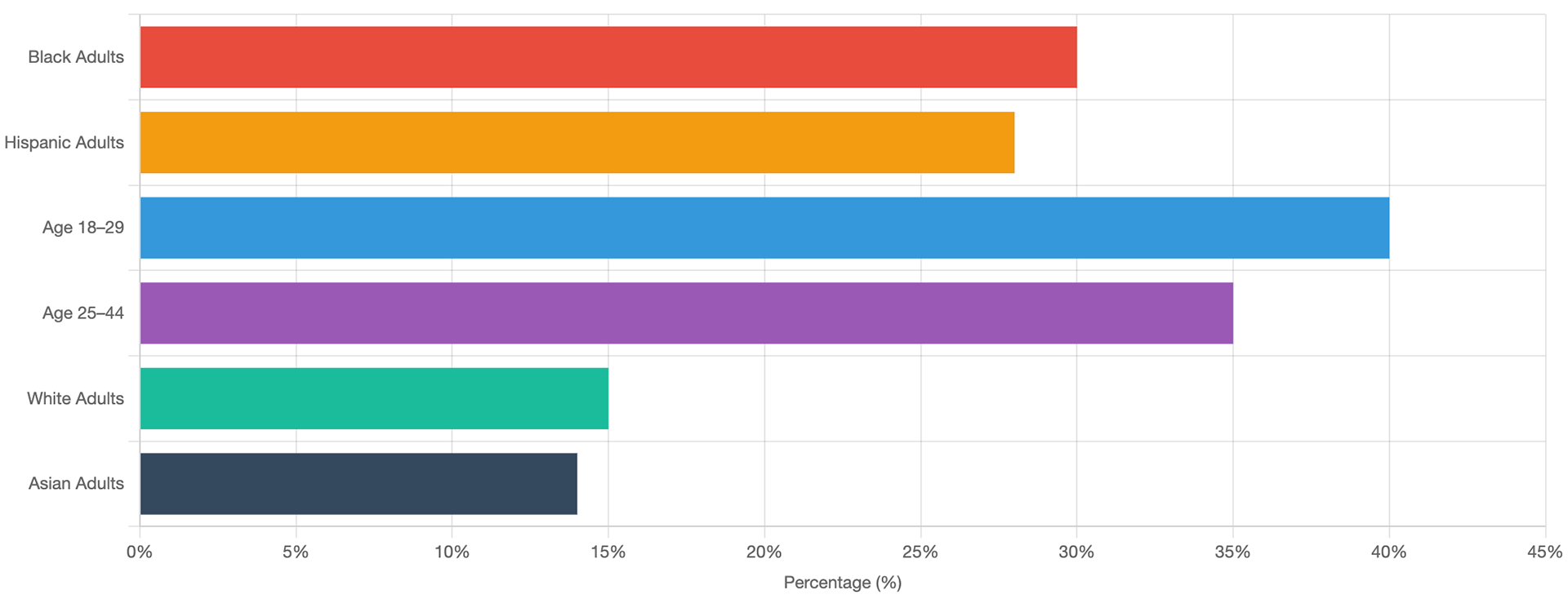

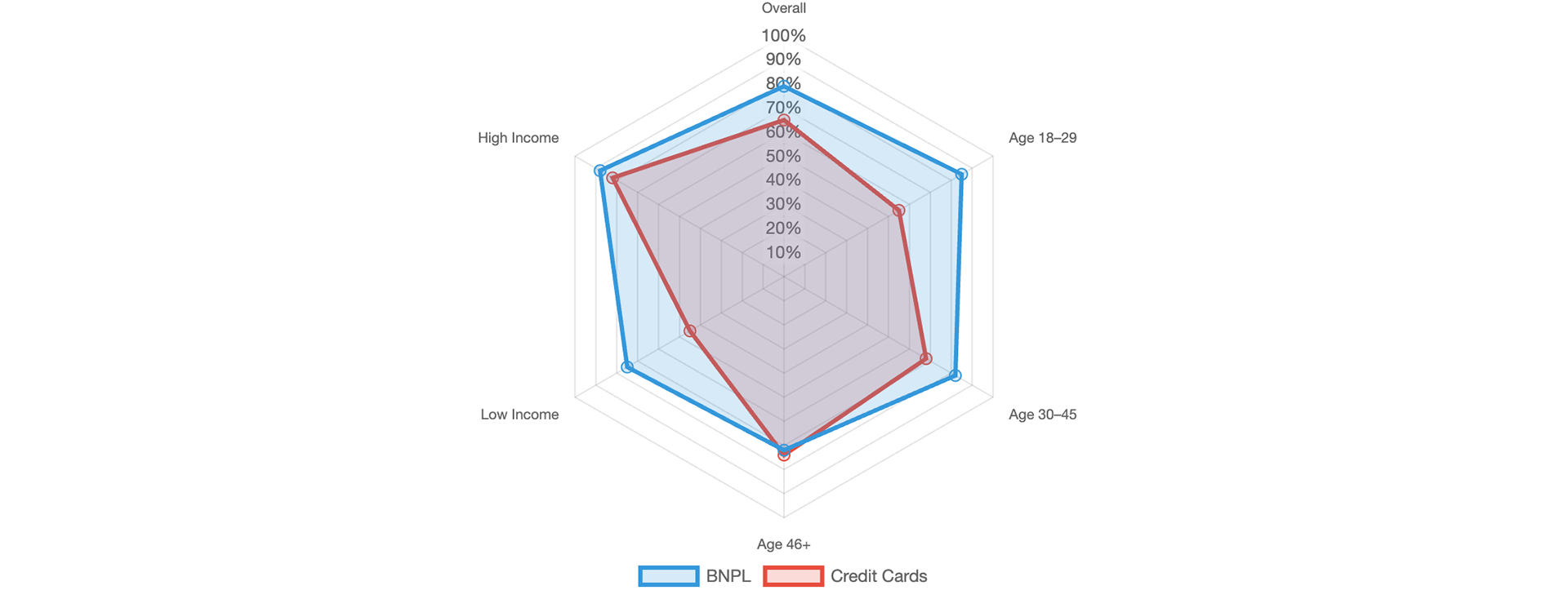

However, beneath success metrics a more complex pattern was emerging. The demographic composition of BNPL users revealed systematic differences from traditional credit users. As documented in the Federal Reserve's 2025 Report on Economic Well-Being, BNPL usage was highest among Black adults (30%), Hispanic adults (28%), and those aged 18-29 (40%), populations that historically faced barriers to traditional credit access. While 79% of BNPL applicants received approval in 2022 compared to just 65% for credit cards, this expanded access came with hidden costs that would only become apparent over time (Capital One Shopping, 2025).

BNPL Usage by Demographics

Percentage of Each Group Using BNPL

Source(s): Berg et al. (2024); Capital One Shopping (2025) for fee comparisons.

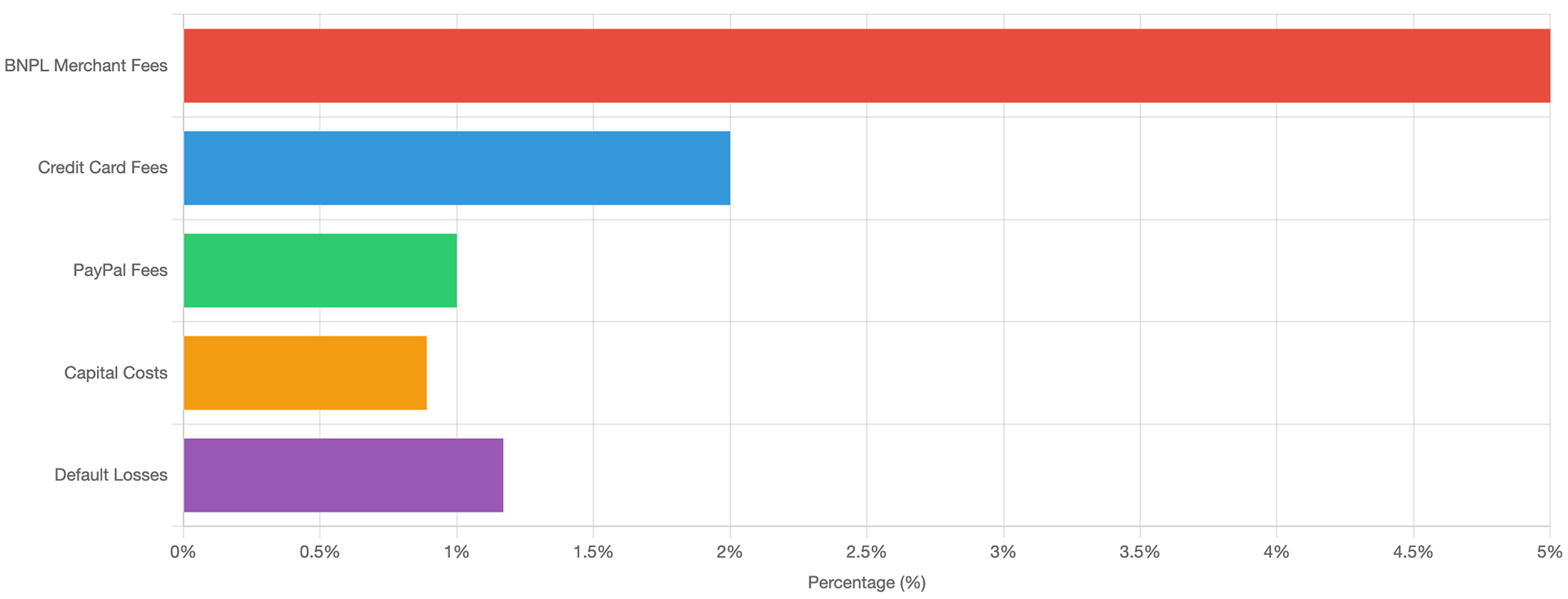

Unlike credit cards where consumers pay interest on carried balances, BNPL providers generate revenue primarily through merchant fees averaging 4-6% of transaction value significantly higher than the 1.5-3% charged by credit card companies (Berg et al., 2024). This merchant-subsidized model created what behavioral economists recognize as a "pain of payment" reduction that fundamentally altered consumer psychology around purchasing decisions. Merchants prefer this due to the cart abandon rate reducing as well as the increase in potential sales. Default rates however are perceived riskier than credit cards rolling nature of credit.

BNPL Cost Structure for Merchants

Percentage of Transaction Value

Source(s): Capital One Shopping (2025)

Part II: Long-Term Impacts on Consumer Financial Health and Market Dynamics

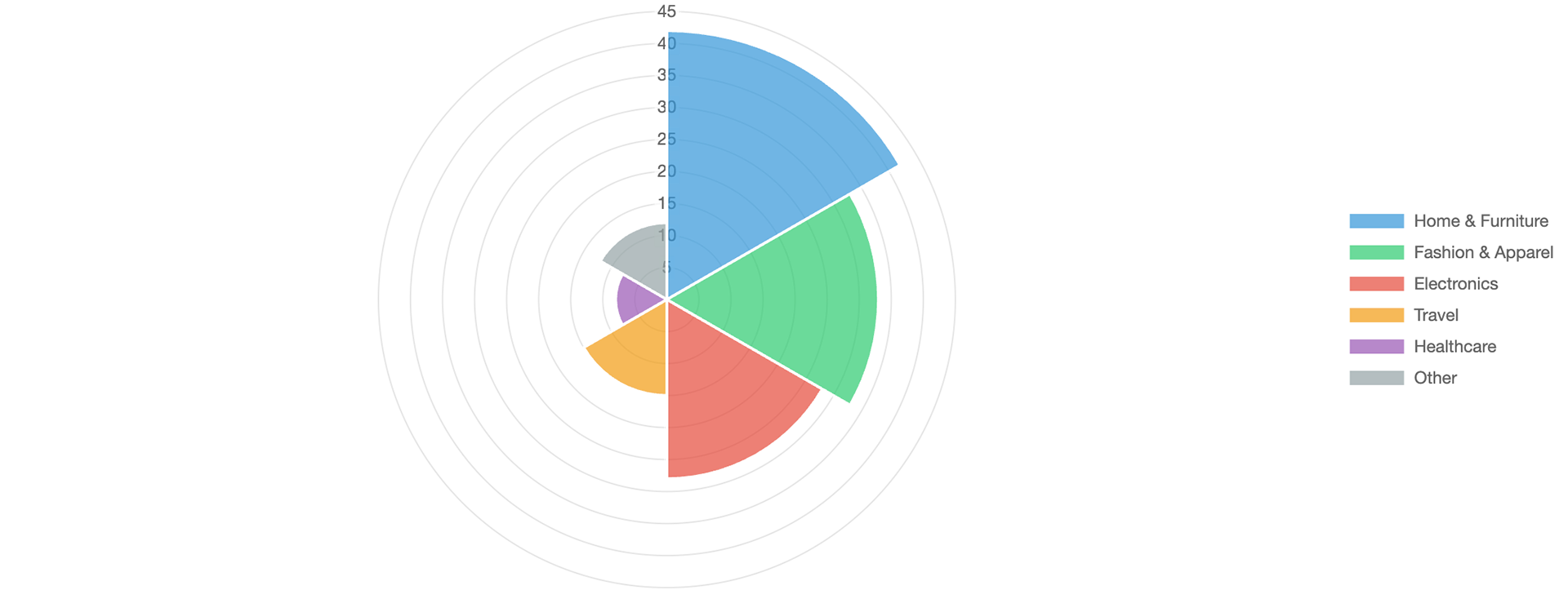

Initial BNPL usage typically coincides with a specific purchase need, 42% of users report their first BNPL transaction was for home furnishings or appliances (Capital One Shopping, 2025). The seamless checkout experience and interest-free structure create positive reinforcement, leading to expanded usage across categories. Within six months, the average BNPL user maintains 2.7 active loans across different providers, a phenomenon researchers term "loan stacking" that remains largely invisible due to limited credit bureau reporting requirements.

The psychological dimensions of BNPL usage reveal why traditional financial literacy interventions prove ineffective. As documented in the time-inconsistency framework developed by researchers at the Journal of Theoretical and Applied Electronic Commerce Research (2025), BNPL exploits present bias by making "future costs less salient than immediate benefits." The mental accounting separation between the purchase decision and payment obligation reinforced by BNPL marketing that emphasizes "budgeting" rather than "borrowing" creates what behavioral economists call a "cognitive decoupling" that increases spending beyond sustainable levels.Das (2024) provides crucial evidence on the well-being implications of sustained BNPL usage. Using nationally representative data from the Survey of Household Economics and Decision making (2021-2023), the research reveals that BNPL users report financial well being scores averaging 4.2 compared to 6.1 for non-users on a 10-point scale. While this raw difference of -1.9 points reduces to -0.3 after controlling for pre-existing financial constraints, income, and credit access, the persistence of negative associations even after extensive controls suggests BNPL usage may exacerbate rather than alleviate financial stress.

BNPL Usage by Purchase Category

Percentage of BNPL Transactions

The Federal Reserve's 2025 consumer credit data reveals that revolving credit growth slowed to 1.8% annually during 2023-2024, the lowest rate since 2010, while BNPL transaction volumes grew at 27% annually over the same period.

The response from financial institutions has reshaped the consumer credit landscape. Major banks launched their own BNPL offerings such as Chase's "My Chase Plan," Citi's "Flex Pay," and American Express's "Plan It" but struggled to match the point-of-sale integration and merchant partnerships that gave BNPL providers such as Affirm or Klarna their competitive advantage. This fragmentation of the consumer credit market created what economists term a "regulatory arbitrage" opportunity, where functionally similar credit products face vastly different oversight requirements.

The systemic risk implications of widespread BNPL adoption remain underappreciated by regulators focused on institution-level oversight. With BNPL loans typically unreported to credit bureaus, the $109 billion in outstanding BNPL obligations as of 2024 represents what researchers term "phantom debt" credit exposure invisible to other lenders and absent from systemic risk calculations. The interconnections between BNPL usage, traditional credit utilization, and banking system stability create feedback loops that amplify financial stress during economic downturns.

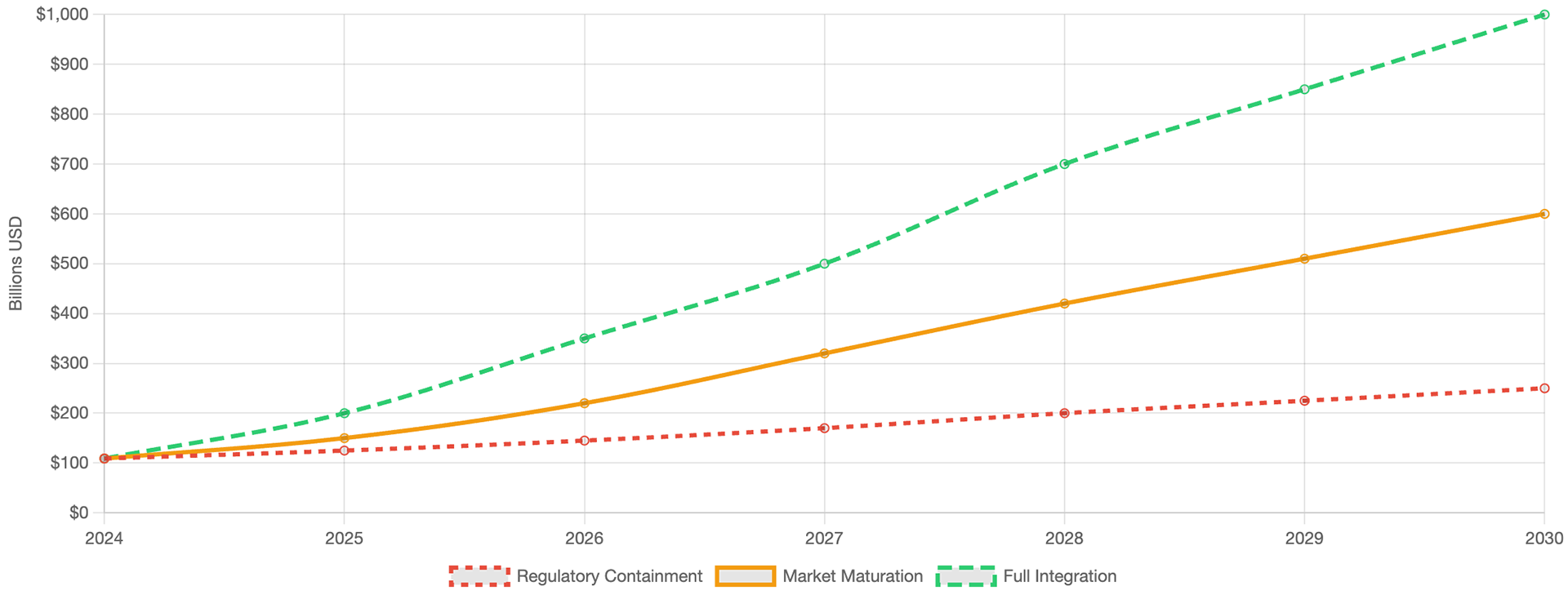

BNPL Market Projections: Three Scenarios to 2030

Global Transaction Volume (Billions USD)

Part III: Divergent Futures - Projecting BNPL's Trajectory Through 2030

The future evolution of BNPL markets hinges on the complex interplay between technological innovation, regulatory intervention, consumer behavior adaptation and financial market. Based on current trends and emerging patterns, we project three distinct scenarios for BNPL's development through 2030, each with profoundly different implications for consumer welfare and market structure.

Scenario 1: Regulatory Containment and Market Stabilization

The first scenario envisions comprehensive regulatory intervention following the model established by the UK's Financial Conduct Authority and Australia's recent legislative proposals. Under this framework, BNPL providers would face requirements similar to traditional credit providers: mandatory credit checks, standardized disclosure requirements, caps on late fees, and full reporting to credit bureaus. The Consumer Financial Protection Bureau's 2024 interpretive rule classifying BNPL as credit represents an initial step toward this regulatory convergence.

In this scenario, market growth decelerates significantly as compliance costs increase and approval rates decline. We project BNPL transaction volumes would reach $250 billion globally by 2030, representing a 129% increase from 2024 levels but far below the 600%+ growth rates of the early 2020s. The consumer base would shift toward higher-creditworthiness segments as providers implement stricter underwriting standards. Default rates would stabilize at 2-3%, comparable to credit cards, while the average transaction size increases to $200-250 as providers focus on larger purchases to offset higher operational costs.

Scenario 2: Continued Growth and AI-Ecosystem Integration

The second scenario projects organic market evolution without dramatic regulatory intervention, following the path of previous financial innovations like credit cards and online payments. BNPL providers mature into full financial platforms, expanding beyond point-of-sale credit into savings accounts, investment products, and financial management tools. The super-app model pioneered in Asia, as documented by Bian et al. (2024), provides the template for this evolution. Klarna, with their recent IPO, aims to achieve in this field.

Transaction volumes under this scenario reach $600 billion globally by 2030, with BNPL accounting for 12-15% of all e-commerce transactions and 5-7% of in-store purchases. The technology stack evolves to enable real-time risk assessment using alternative data sources social media activity, device usage patterns, and transaction histories creating more nuanced underwriting models that expand access while managing risk. Blockchain integration enables portable credit histories and reduces fraud, while AI-driven financial coaching helps consumers manage multiple BNPL obligations.

The competitive landscape features intense platform competition as BNPL providers, e-commerce giants, and traditional banks vie for customer relationships. Amazon's acquisition of Affirm (hypothetically projected for 2027) and Apple's launch of "Apple Pay Later Plus" shared the rise of commerce and credit. Merchant fees stabilize at 3-4% as competition and scale efficiencies offset risk costs. Consumer outcomes diverge based on financial sophistication, with digitally native users leveraging BNPL as a cash flow management tool while vulnerable populations continue experiencing debt stress.

Scenario 3: Transformation and Full Financial Integration

The most disruptive scenario envisions BNPL catalyzing a fundamental transformation of consumer finance, analogous to how smartphones transformed communication. Central Bank Digital Currencies (CBDCs) enable programmable money with built-in BNPL functionality, while decentralized finance protocols create peer-to-peer BNPL markets without traditional intermediaries. The distinction between payments and credit dissolves as all transactions become potentially deferrable based on real-time financial optimization algorithms.

In this transformed landscape, BNPL transaction volumes exceed $1 trillion globally by 2030, but the metric itself becomes obsolete as deferred payment options embed universally across the financial system. Traditional credit scores give way to dynamic financial health scores updated in real-time based on income flows, spending patterns, and economic conditions. AI agents negotiate payment terms automatically, optimizing across multiple objectives including cash flow smoothing, reward maximization, and credit utilization.

The societal implications prove double edged: financial flexibility reaches unprecedented levels, enabling consumption smoothing that increases overall welfare for disciplined users, while algorithmic optimization of spending creates new forms of digital dependency. Income inequality effects amplify as those with stable earnings and financial sophistication capture the benefits while precarious workers face algorithmic discrimination.

Approval Rates: BNPL vs Traditional Credit Cards

Percentage of Applications Approved

Conclusion: Navigating the BNPL Paradox

The short-term benefits documented in early research increased purchasing power, merchant sales growth, and financial inclusion give way to longer-term challenges including persistent debt cycles, market fragmentation and systemic risk accumulation. The 24% of BNPL users who experience payment difficulties within 12 months represent not edge cases but predictable outcomes of a business model that profits from reducing the psychological barriers to debt accumulation.

For policymakers, the challenge lies in preserving BNPL's genuine innovations, transparent pricing and expanded access while mitigating its harmful effects. The evidence strongly supports mandatory credit reporting, standardized disclosures, and caps on loan stacking, but heavy handed regulation risks eliminating the features that made BNPL attractive to underserved populations.

Merchants face strategic decisions, while the 20% sales lift documented by Berg et al. (2024) appears compelling, the long-term effects on customer relationships, brand perception and pricing strategy require careful consideration. Some merchants might opt to finance the deals themselves if regulatory is loose.

For consumers navigating the BNPL landscape requires a fundamental shift in financial literacy education. Traditional warnings about credit card debt prove ineffective when BNPL marketing emphasizes "budgeting" and "financial wellness." New educational approaches must address the cognitive biases BNPL exploits present bias, mental accounting, and social proof while providing practical tools for managing multiple payment obligations across platforms.

The research agenda moving forward must address critical gaps in our understanding of BNPL's long-term impacts. Longitudinal studies tracking cohorts of BNPL users over 5-10 year periods would reveal whether early financial stress indicators persist or resolve as users gain experience. Overseas data needs to be taken into consideration as adoption increases overseas.

As we project forward to 2030 and beyond, the path chosen whether regulatory containment, market evolution, or transformative integration will shape not just payment methods but the fundamental relationship between individuals and money in the digital age.

References

Berg, T., Burg, V., Keil, J., & Puri, M. (2024). The economics of "buy now, pay later": A merchant's perspective. Journal of Financial Economics, 171, Article 104094.

Bian, W., Cong, L. W., & Ji, Y. (2024). The rise of e-wallet super-apps and buy-now-pay-later (NBER Working Paper No. 33178). National Bureau of Economic Research.

Capital One Shopping. (2025). Buy now pay later statistics (2025): Market share & trends. Retrieved from https://capitaloneshopping.com/research/buy-now-pay-later-statistics/

Das, V. (2024). Buy now, pay later (BNPL) use and perceived financial well-being. SSRN Electronic Journal. https://dx.doi.org/10.2139/ssrn.4957294

deHaan, E., Kim, J., Lourie, B., & Zhu, C. (2024). Buy now pay (pain?) later. Management Science, 70(8), 5586-5598.

Demand Sage. (2025). 21 buy now, pay later (BNPL) statistics for 2025. Retrieved from https://www.demandsage.com/bnpl-statistics/

Federal Reserve Board. (2025). Report on the economic well-being of U.S. households in 2024 - May 2025. Board of Governors of the Federal Reserve System.

Journal of Theoretical and Applied Electronic Commerce Research. (2025). Adoption of buy now, pay later (BNPL): A time inconsistency perspective. Journal of Theoretical and Applied Electronic Commerce Research, 20(2), 81.

Kumar, S., et al. (2024). The effects of buy now, pay later (BNPL) on customers' online purchase behavior. Journal of Retailing, 100(3).